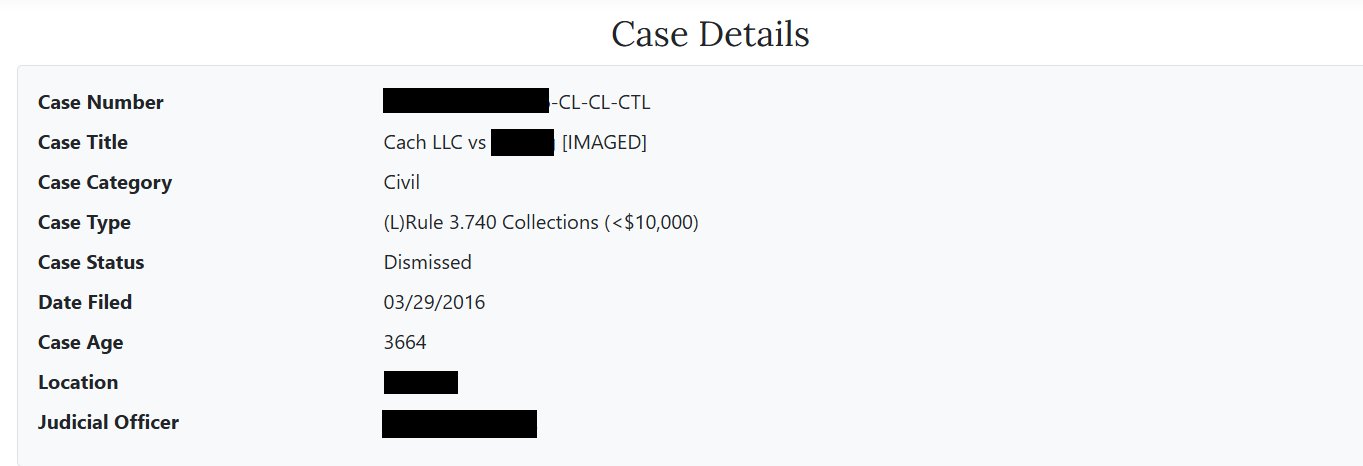

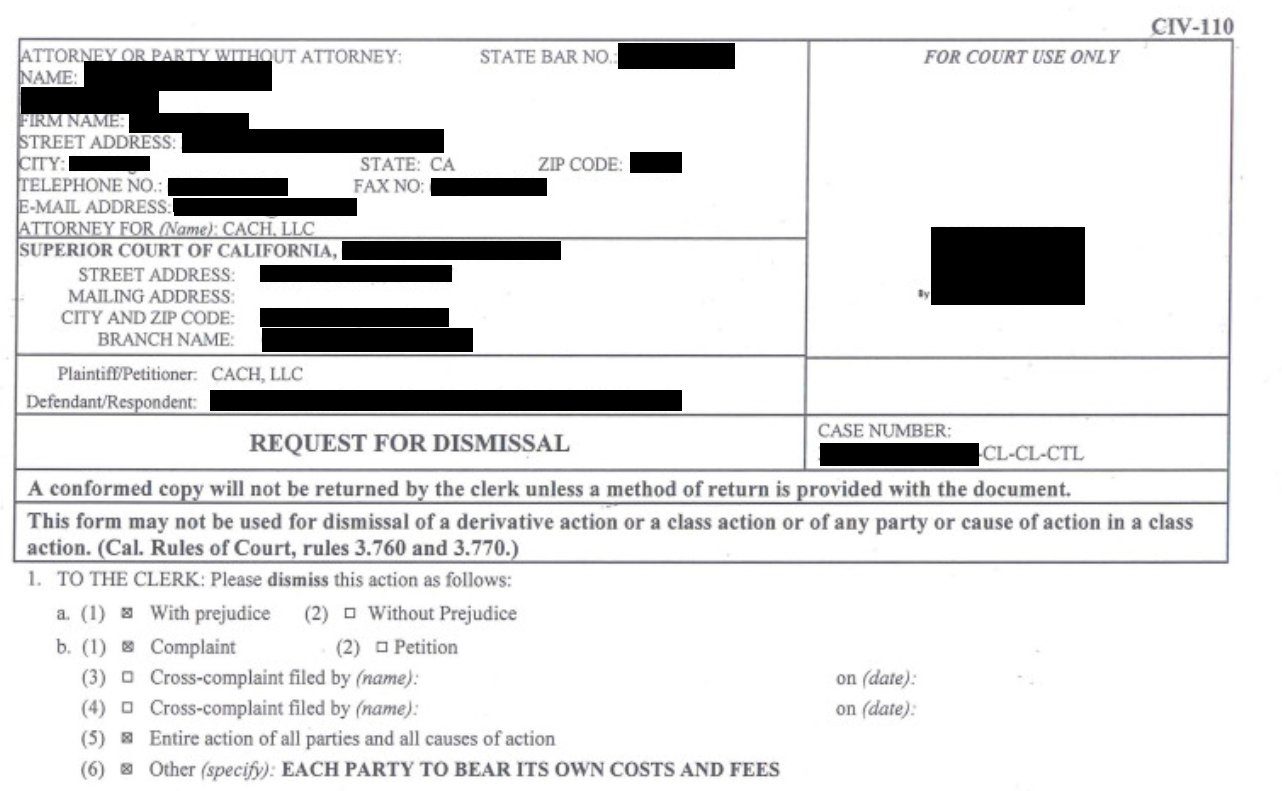

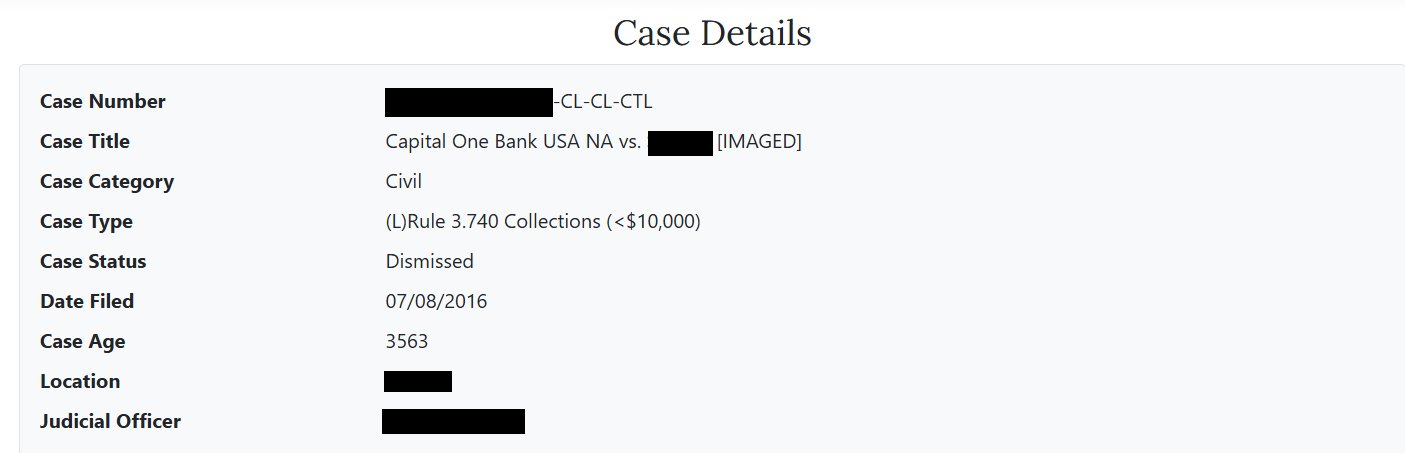

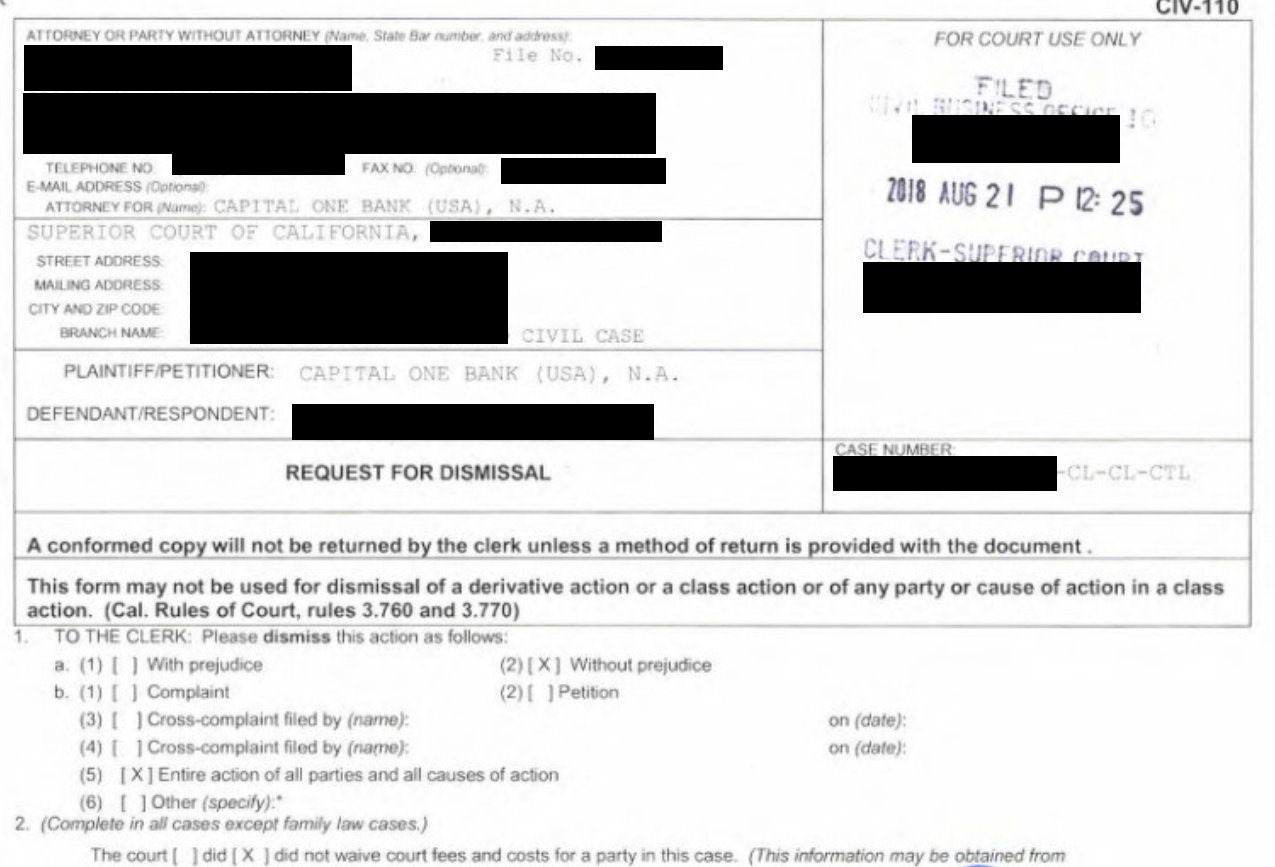

I was served with a debt collection lawsuit in California. Then it happened again. The first case was filed by a professional debt buyer backed by a law firm that runs hundreds of these cases through California courts every month. The second came from the original creditor itself, a national bank with its own in-house collections team.

I had no legal background. I had no lawyer. I had a deadline, a stack of papers I didn't understand, and a lot of late nights reading California code on leginfo.ca.gov.

I won both cases. Not by luck, but by learning exactly how these cases work and where they fall apart.

I learned what the collectors have to prove, where their cases collapse under the weight of their own paperwork, and which procedural tools give defendants real leverage. This kit is everything I learned, organized so you can move fast from day one.

Chris, California